Credit scores have been steadily rising since the Great Recession, averaging over 700 for the first time ever. But if you're not there yet, there is good news.

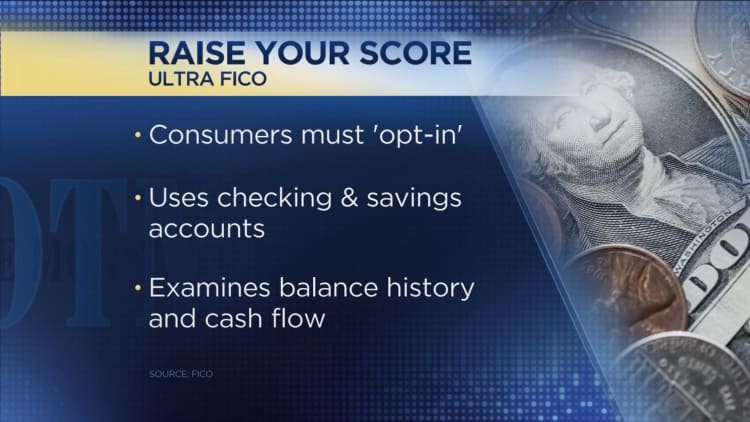

New criteria will weigh how you manage the cash in your checking and savings accounts, which means the good financial habits you practice today can have a direct effect on your score. Some of the mistakes that may have dogged you in the past will have less of an impact on your creditworthiness.

Credit scores, notably those from FICO, one of the largest credit scoring companies, range from 300 to 850. The three-digit number is designed to predict risk — specifically, the likelihood that you will become seriously delinquent on your credit obligations or default.

That score plays a big role in your daily life. It can determine the interest rate on your credit cards, car loan and mortgage — or whether you can get a loan at all.

Recently, Experian announced a program called Experian Boost rolling out this year that allows consumers to influence their credit scores by showing on-time payments for utilities, phones and cable TV.

If you agree to give Experian permission to access your bank accounts, it can factor those payments into your credit history, immediately improving your score. (You can sign up now for Experian Boost to get early access to the program.)

Roughly 8 million people could potentially move into the fair (580-669) or good (670-739) credit ranges under the new system, according to research by Experian.

That's on the heels of another pilot program set to roll out this year from FICO, called UltraFICO. It's designed to give people with dings on their credit histories a chance to have their banking activity considered as well, including how long accounts have been open and evidence of saving.

Close to 4 million consumers could see an increase of 20 points or more under that new plan, according to David Shellenberger, senior director of scores and predictive analytics at FICO.

And because of improved standards for utilizing new and existing public records implemented last year, the three major credit reporting companies are now excluding all tax liens from credit reports. That also sent some scores higher, for some by as much as 30 points.

All of these changes give lenders a greater pool of potential borrowers to draw from, particularly those who fall in the gray area in terms of credit scores — the upper 500s to lower 600s — or who have a limited history or previous financial distress.

At the same time, credit card interest rates have never been higher, setting the stage for potential problems for some consumers.

Looser standards might mean there's a chance more people will take on more debt than they can afford, according to Tim Devaney, a credit card expert at Credit Karma.

The average card interest rate is currently at a record 17.41 percent, according to CreditCards.com's latest report. That's up from 16.15 percent one year earlier and 15.22 percent two years ago.

Despite the dangers of high-interest loans, the number of credit card accounts in the U.S. is rising quickly.

About 75 percent of Americans now have at least one credit card, and the average credit card balance is roughly $6,375, up nearly 3 percent from last year, according to Experian's annual study on the state of credit and debt in America. Total credit card debt has reached its highest point ever, surpassing $1 trillion, according to a report by the Federal Reserve.

As always, financial pros warn consumers to be careful.

"Just because somebody will lend you money doesn't mean you should take it," said Matt Schulz, chief industry analyst at CompareCards.com.

Good credit card management boils down to making payments on time and in full, keeping balances low on credit cards and other revolving credit and applying for new cards only as needed.

"If you do those three things, your credit is going to be just fine," Schulz said.

"On the Money" airs on CNBC Saturdays at 5:30 a.m. ET, or check listings for air times in local markets.

More from Personal Finance:

Beware: If you're running up a tab on plastic, credit card interest rates are at record highs

Your credit score may have just jumped. Here's why

You're probably using the wrong credit card. How to fix that